Why Should Financial Institutions Avoid Black-Box IFRS 9 Solutions?

Is Your IFRS 9 Process a Black Box? Uncover the hidden complexities for clearer, more effective credit risk decisions.

As more Financial Institutions are implementing IFRS 9 Expected credit loss models, many are turning to third-party “black-box” solutions. IFRS 9 is very crucial for FIs as it directly impacts profitability. Therefore, the ECL modeling process must be transparent and well-defined. These solutions often promise simplicity but can introduce significant challenges. This article explores the challenges of relying on black-box solutions, provides examples of their pitfalls, and suggests more transparent, flexible alternatives.

Challenges of relying on IFRS 9 black-box solutions:

1) Senior management and decision-makers frequently do not understand the code or calculations driving the ECL estimates, risking misinformed decisions.

2) Many teams are accustomed to spreadsheet-based models. Complex user interfaces designed by solution providers can be unintuitive, limiting proper analysis.

3) Some solutions merely multiply PD, LGD, and EAD while overlooking components estimation methodologies, such as TTC PD/LGD, macroeconomic modeling, PiT adjustments, staging, and SICR.

4) Step-by-step visibility into ECL modeling vital for assessing portfolio behavior is often missing. Users directly receive a final number without understanding how it was derived.

5) Usually, the solutions are harder to integrate and require system and hardware enhancements to work efficiently.

6) Usually, black box IFRS 9 solutions increase the cost and reduce control over the ECL estimation.

7) Sometime, adjusting assumptions or adding expert judgment can be difficult to integrate into the solution.

Examples of Black-Box Systems Shortcomings:

EXAMPLE # 1 Lack of Transparency

The first example is related to the black box solution Mechanism itself. You give input, set the parameters and run the solution, and receive final ECL numbers without clarity on:

· The specific model used

· Key parameters driving the outcome

· Whether the approach is suited to your portfolio

· How to incorporate management overlays

These are questions which are not addressed in the solutions by solution providers.

EXAMPLE # 2 Inability to Perform Data Analysis

When using these solutions, conducting thorough data analysis to understand your portfolio's behavior becomes extremely challenging. Key insights, such as the macroeconomic impact on Expected Credit Loss (ECL), forward-looking Point-in-Time (PiT) Probability of Default (PD) fluctuations, recovery trends, and default behaviors, are difficult to obtain. This limitation arises because users lack access to the ECL modeling steps, which are crucial for gaining deeper analytical insights.

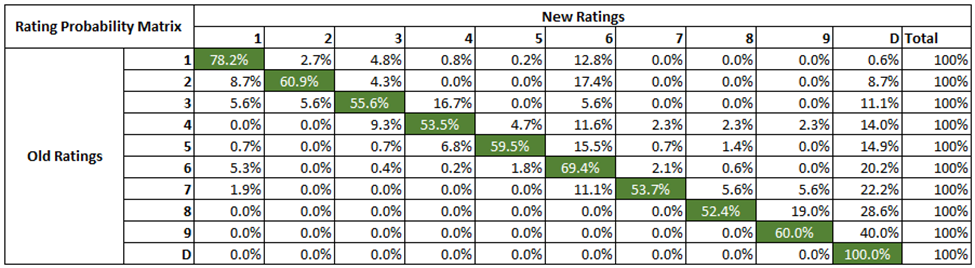

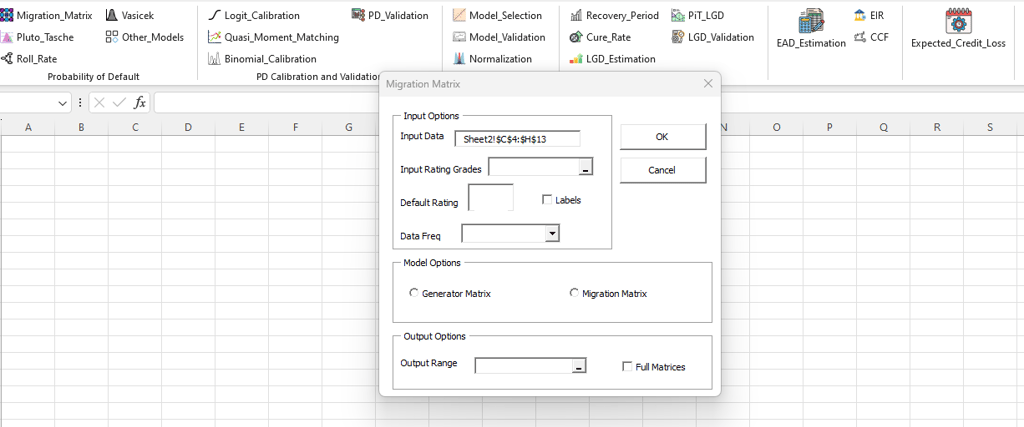

Let’s take an example of TTC PD estimation for corporate portfolio using Markov Chain Migration Matrix

In the image above, you can see a probability matrix that not only provides TTC PDs but also offers valuable insights into both the model and portfolio:

1) The first key insight is that the rating model is performing effectively, as indicated by the diagonal dominance in the transition matrix. This means that all diagonal elements of the transition matrix are larger than the corresponding row sum of off-diagonal elements the matrix.

2) The matrix also provides a clear view of the percentage of obligors that experience rating upgrades or downgrades. This information will help management or analyst to understand how much notch downgrade is actually a significant increase in credit risk for each rating grade.

3) Additionally, the matrix highlights forward transition probabilities. If these probabilities are increasing, it indicates a deterioration in portfolio credit quality.

These valuable insights are often missing when using IFRS 9 solutions because users only have access to the final output PD rather than the underlying modeling process.

Practical Solutions

Financial Institutions have several options to avoid black-box limitations:

SOLUTION # 1 Advisory Services & Custom Automation

Financial institutions can utilize advisory services, gaining access to the following benefits:

1) Appropriate Models tailored to each portfolio.

2) Working in a familiar environment ensures management and decision-makers understand the modeling steps.

3) Each calculation is transparent, enabling more effective data analysis.

4) Management overlays can be seamlessly integrated for greater flexibility.

Once an FI is confident in the approach, solutions can be automated in VBA, R, Python, or another language of choice allowing flexibility and reducing long-term costs.

How Probmatrix Helps:

At Probmatrix, we specialize in both IFRS 9 advisory and automation. Our cost-effective services give your FI full control over the ECL modeling process:

1) No hidden codes or complex interfaces every stage is clearly documented.

2) Instead of complex UI-based systems designed for solution providers, our approach prioritizes user-friendliness and integration with tools your team already knows.

3) We incorporate TTC PD, TTC LGD, macroeconomic modeling, PiT estimates, SICR, and staging mechanisms.

4) Our solution provides step-by-step visibility into ECL estimation, allowing management to track portfolio behavior, detect stage movements, and make informed strategic decisions not just rely on a single output number.

5) Our approach is lightweight and designed to work within your current infrastructure, saving you time and reducing costs.

6) Keeps your organization in full control of IFRS 9 compliance. No hidden dependencies, no unnecessary outsourcing, just a solution designed for your needs.

7) Incorporate expert judgment without struggling with system limitations or hidden processes.

SOLUTION # 2 Probmatrix Add-In

Our Excel Add-in provides an intuitive ribbon interface for comprehensive modeling and data analysis. It includes multiple methodologies for PD, LGD, macroeconomic modeling, and EAD, plus validation tools.

KEY BENEFITS:

1) Works like any native Excel feature.

2) Reduces time and effort.

3) Supports multiple methodologies based on portfolio needs.

4) It also contains data analysis tools.

5) Displays each calculation step, making the process easy to review and audit.

6) Can be customized based on requirements.

Conclusion

Black-box IFRS 9 solutions may appear convenient, but their hidden methodologies, limited transparency, and integration challenges often create more problems than they solve. Financial Institutions stand to benefit from a clear, step-by-step approach that not only fulfills regulatory obligations but also empowers management with meaningful insights. Whether you need complete advisory and automation, simple Excel-based tools, or an easy-to-use Add-in, the right solution should always offer visibility, flexibility, and full control over your IFRS 9 compliance.

For more information on how Probmatrix can help, feel free to reach out. Let’s make IFRS 9 compliance both transparent and straightforward.

Expert risk management tools and consulting services.

Contact

info@probmatrix.io

+92 336 5264744

© 2025. All rights reserved.

Risk Matrix